It is a financial statement prepared by all types of businesses (sole proprietors, partners, enterprise, etc.) at a given date. The balance sheet represents the financial position of a business at any given point in time. It shows the company’s assets along with how they are financed, which may be by debt, equity, or a combination of both.

Financial Statements can be presented in two ways; Vertical Representation or Horizontal Representation.

Few other names of a balance sheet are Statement of Financial Position, Statement of Financial Condition or Statement of Net Worth.

It is based on a fundamental accounting equation which is;

Assets = Liabilities + Equity

The above equation means that at any point in time, a business’s assets should be equal to its liabilities and equity. Usually, the balance sheet is prepared from a trial balance.

The three aspects of a balance sheet are:

The Balance sheet presents an account of where a company has obtained its funds and where it has invested them. A business has primarily two sources of funds which are shareholders and lenders. These funds are then invested in assets which helps the business in generating revenue.

Related Topic – Can Assets have a Credit Balance?

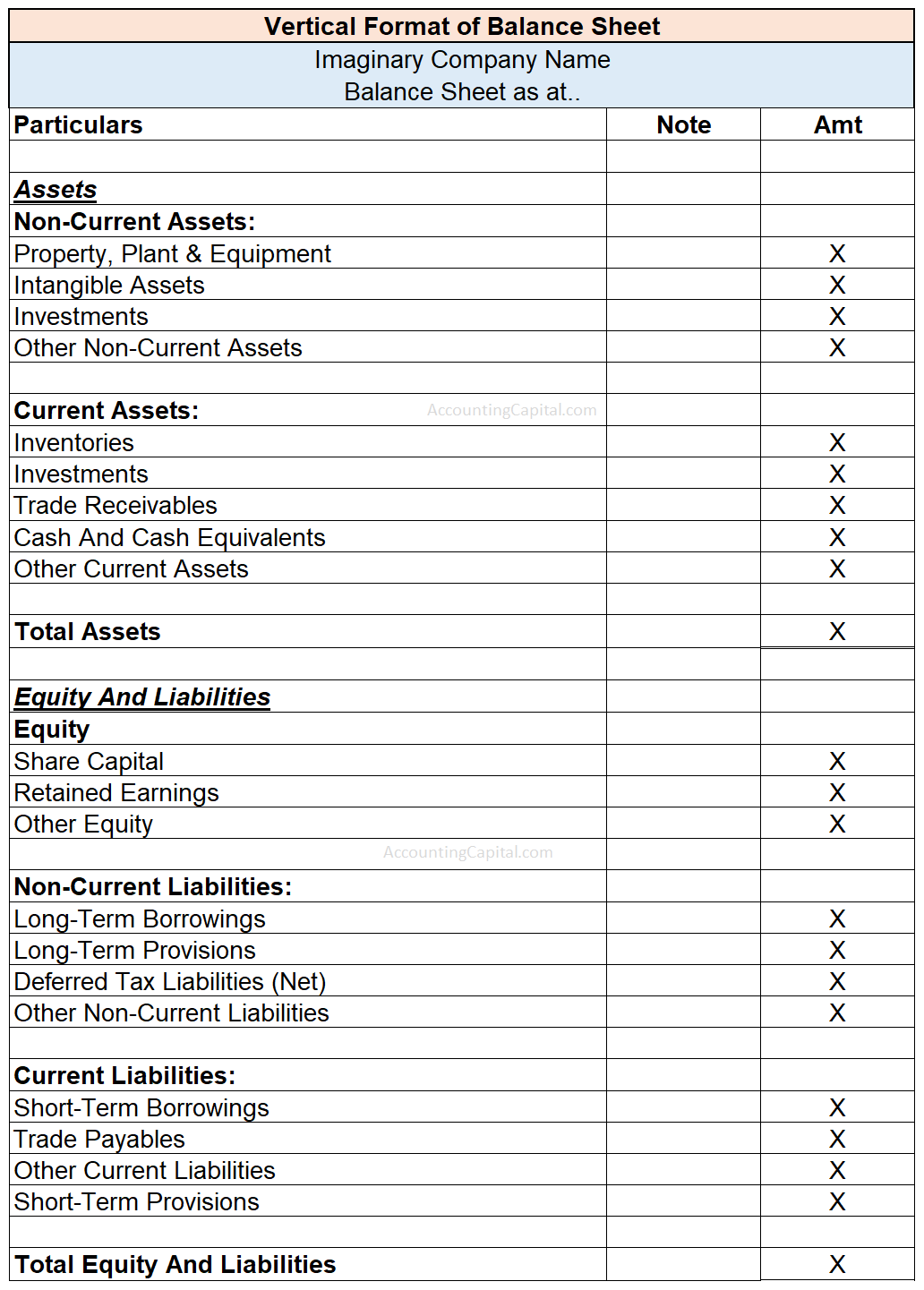

The vertical format is also known as the report format. This presentation starts with assets and after that, equity & liabilities are listed. The format is categorized into sections that are in descending order of liquidity, which means prioritizing items that are less liquid in nature. The data is presented from top to bottom in two columns i.e. assets and liabilities in one column and amounts in another.

The five major sections under the vertical format of the Balance sheet are;

There are various advantages of a Vertical format balance sheet.

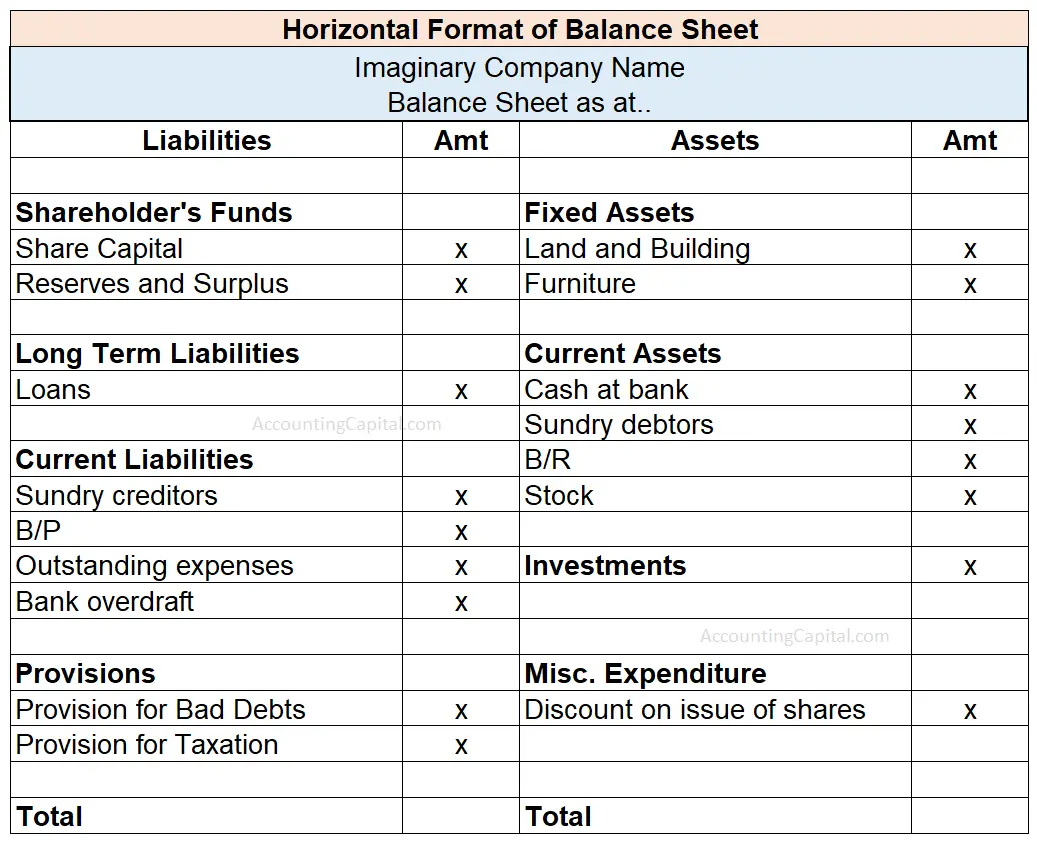

Horizontal format lists all liabilities on the left-hand side and all assets on the right-hand side of the balance sheet. It is also called a T-shaped Balance sheet.

In a horizontal format, assets and liabilities are presented descriptively. The liabilities and assets are listed in the 1st and 3rd column of the balance sheet respectively whereas, the amounts associated with them are listed in the 2nd and 4th columns respectively.

This format is not ideal for both inter-firm and intra-firm comparisons because the information presented only relates to the current year. It is easier to compare the information in a vertical format balance sheet.

The balance sheet is the most important source of information about a company’s financial health. By analyzing the components of the balance sheet you can;

Grouping refers to putting similar items with similar qualities together and showing them under a common head inside financial statements. For example, all the debtors of an organisation are grouped together under just 1 head of sundry debtors in the balance sheet. Similarly, Inventory shows the net total of Raw Material, Work In Progress and Finished Stock.

Marshalling refers to the arrangement of assets and liabilities on the balance sheet in a particular order. The assets and liabilities are shown in a logical order for helping the stakeholders in understanding the financial statements easily.

There can be 3 ways of marshalling;

Under this method, the assets & liabilities are shown in the order of their liquidity or urgency of payment i.e. assets & liabilities which are highly liquid, like Cash equivalents, Bank overdraft, etc. are shown first & permanent assets & liabilities like Land & Building, Capital, etc. are shown afterwards.

The following is a format of a balance sheet based on this order.

| Balance Sheet – In order of Liquidity | |||

| Liabilities | Amt | Assets | Amt |

| Creditors | x | Cash | x |

| Loans | x | Bank | x |

| Reserves & Surplus | x | Debtors | x |

| Capital | x | Furniture | x |

| Plant & Machinery | x | ||

| Building | x | ||

2. In Order of Permanence

Under this method, the assets & liabilities are shown in the order of their permanency or duration i.e. permanent assets & liabilities like Land & Building, Capital, etc. are shown first & the current assets & liabilities like Cash, Debtors, Creditors, etc. are shown afterwards.

The following is a format of a balance sheet based on this order.

| Balance Sheet – In order of Permanence | |||

| Liabilities | Amt | Assets | Amt |

| Capital | x | Building | x |

| Reserves & Surplus | x | Plant & Machinery | x |

| Loans | x | Furniture | x |

| Creditors | x | Debtors | x |

| Bank | x | ||

| Cash | x | ||

3. Mixed Order

Under this method, the assets are arranged in the order of liquidity & the liabilities are arranged in the order of permanency.

The following is a format of a balance sheet based on this order.

| Balance Sheet – Mixed order | |||

| Liabilities | Amt | Assets | Amt |

| Capital | x | Cash | x |

| Reserves & Surplus | x | Bank | x |

| Loans | x | Debtors | x |

| Creditors | x | Furniture | x |

| Plant & Machinery | x | ||

| Building | x | ||